By Rene Anthere Rwanyange

Rwanda’s financial sector remained resilient in 2025, sustained by a favourable macroeconomic environment and robust institutional performance, the latest Monetary Policy and Financial Stability (MPFSS) shows.

According to the MPFSS statement released by the National Bank of Rwanda total assets across the sector grew by 23.7 percent to reach Rwf15.9 trillion by December 2025, reflecting strong expansion across all segments.

Lending institutions, including banks and microfinance institutions, recorded solid growth, supported by rising deposits, capital injections, and improved operational resilience.

The banking sector continues to dominate the financial system, accounting for 67 percent of total assets. Of the country’s 11 banks, eight are foreign-owned, holding 52.6 percent of banking assets, while three domestically owned banks account for 47.4 percent.

However, the sector remains concentrated, with the five largest banks controlling 72.9 percent of total assets. Banks are required to maintain adequate liquidity levels to meet customer demands, particularly during periods of financial stress, the regulator said.

Fraud cases drop despite rising Cyber threats

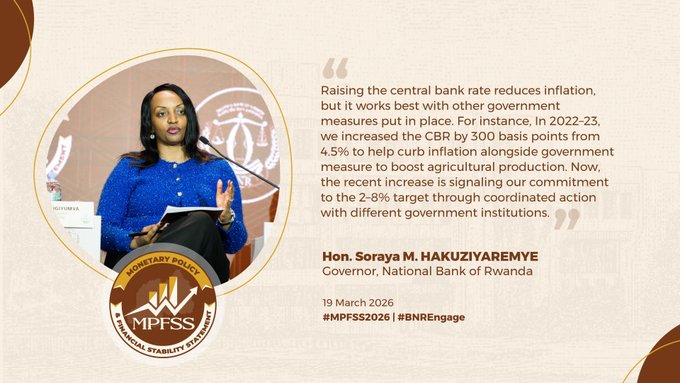

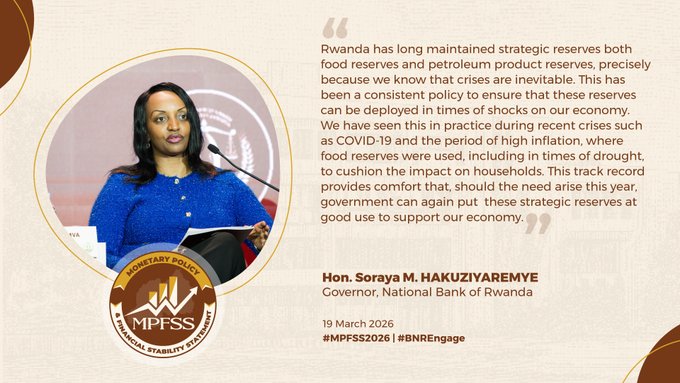

Meanwhile, digital fraud in the financial services sector has declined significantly, falling by 40 percent over the past two years, from 5,000 cases to 3,000; according to central bank Governor Soraya Hakuziyaremye.

Speaking at a press conference following the release of the report on Thursday, March 2026, the Central Bank Governor attributes the decline to strengthened security measures and increased collaboration between regulators and financial institutions.

“Due to the uptake of technology, there are digital fraud cases in the financial services sector. However, over the past two years, the number has reduced… thanks to various protective measures,” she said, noting that fraud risks, like any other theft, couldn’t be entirely eliminated.

The decline comes amid a surge in cyber threats driven by the rapid adoption of digital banking, mobile money, and online financial services. Fraudsters continue to target online banking platforms, payment systems, card transactions, and digital lending applications.

Expanding financial access

Over all, Rwanda’s financial ecosystem has continued to expand, including 11 banks, 70 microfinance institutions, 18 insurance companies, one credit reference bureau, 12 pension schemes, 250 non-deposit-taking financial institutions, 78 foreign exchange bureaus, and 44 payment service providers.

By the end of 2025, banks served 2.3 million depositors and 2 million savings account holders, underscoring their role in promoting formal savings. Lending activity also remained strong, with more than 723,000 borrowers accessing credit.

Persistent challenges in digital finance

Despite progress, challenges persist in the digital financial landscape. A joint study by the central bank and the Consultative Group to Assist the Poor highlights widespread vulnerabilities.

The study found that 44 percent of digital financial services users have suffered financial losses due to cyber-enabled theft, while 84 percent encountered attempted fraud.

Nearly all respondents, 97 percent, reported experiencing at least one technology-related issue, including network failures, system errors, accidental transfers, or data misuse.

Low digital literacy remains a critical concern, with 82 percent of users lacking sufficient understanding of digital financial systems. Additionally, 41 percent reported sending money to the wrong recipient, while 65 percent experienced disputes or service issues involving agents.

Authorities warn that many scams involve impersonation and deceptive messages, often tricking victims into authorising transactions by entering verification codes.

Strengthening consumer protection

The central bank says it is working closely with financial institutions to enhance safeguards and ensure accountability. In cases where fraud is linked to institutional failures, investigations are conducted to determine responsibility, with affected customers eligible for reimbursement.

“Even when money is stolen, we must ensure measures are in place to recover funds and punish those responsible,” Hakuziyaremye said, adding that customers should be reimbursed within no more than seven days.

Regulators have also cautioned that financial institutions failing to implement adequate security measures will be held accountable.